Lump Sum Case Studies

- Ben HC

- Aug 3, 2024

- 15 min read

Updated: Apr 8, 2025

If you haven't already I recommend you first read my article on an approach to lump sums. Now that we have a basic approach, lets apply it to several real cases that I've helped with in the past week. This will help show the benefit of the patient centered approach to maximizing travel rewards from a lump sum or atypical growth in your spending. Note that the specific calculations will differ based on currently available sign up bonuses. For the specific case of tax payments check out my article on the topic.

Disclaimers and referral links at the bottom, as always if you want personalized advice, reach out for a consult.

Case 1 - CAD spend with transaction fee

Case 2 - Non USD foreign spend with no transaction fee, but prefers cashback rewards

Case 3 - Non USD foreign spend across a vacation

Case 4 - USD foreign spend with transaction fee

Note: Since writing this article available offers both listed and unlisted have changed. If you have a large lump sum (in excess of $50k CAD) you would certainly benefit from reaching out to discuss these options.

Case 1 - Equipping the Office

Presenting Complaint

Our patient is equipping an out of hospital OR for dental care and are about to finalize on a quote for an anesthesia gas machine and monitors. There will be other ongoing expenses but this is one of the bigger "lumpier" purchases that will occur for the practice. The expense is in Canadian, but the vendor charges a 2% transaction fee for credit card payments. The items are durable goods that may benefit from extended warranty, but their intended commercial use and specialized nature make them unlikely to be covered by any credit card purchase protection. The estimated cost is $35k for this purchase.

Patient History

This patient already has an Amex Business Platinum and has long ago received the SUB for it. Otherwise they have a personal TD Aeroplan VIP. He values travel and wouldn't mind earning Amex MR, Aeroplan points, Scene+ points, Bonvoy points, or cash back, but would rather not start in a new point ecosystem like Avion or Aventura. They are looking for a 1 or 2 card approach, but don't want to go through the "hassle" of splitting the purchase across a half dozen cards.

Evaluating Treatment Options

Given the nature of the spend as in Canadian, we don't need to account for foreign exchange fees, but will have to make sure that we address the 2% transaction fee drag. Already holding an TD AP VIP they are not eligible for the SUB on the CIBC and Amex versions of this card. They also may not perceive much benefit from adding an Amex Personal Platinum as they already have lounge access and this would block them from a Personal Gold SUB in the future. As an MD they have access to multiple fee rebate options for cards with most of the major banks which lowers their barrier of entry. Also, current publically available offers for the Amex personal gold and TD Business Aeroplan are poor options as they are designed as small monthly bonuses for ongoing spend, but if they're an OMA member, the personal gold offer is a lump sum plus a $50 OMA credit which could be worthy

Establishing the Baseline

Base case in this example would be a debit or wire transfer of the exact amount, a cost of $35k CAD.

Single Card Option

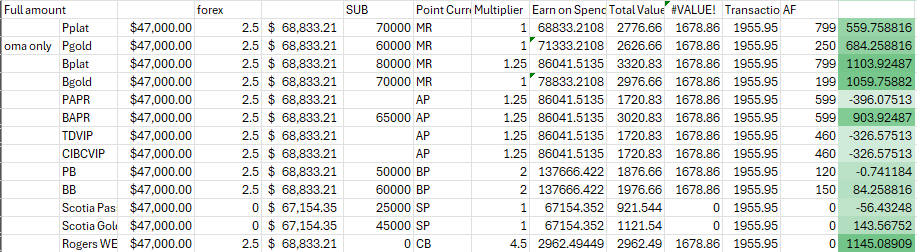

The easiest option to implement is a single card approach where you open just one card and place the total amount on it. This avoids the need to split the purchase and allows you to access card based purchase protections if relevant. Considering the above context we have the below comparison (blocked SUBs and non targeted rewards cards hidden)

Compared to the base case, opening an Amex Business Gold and putting the whole purchase on it leads to a net benefit of $1415 represented by a transaction cost of $700, annual fee of $199, and ~115K Amex MR. The Business Gold's performance is boosted by a high SUB, low annual fee and its unique recurring quarterly bonus reward of 10k MR for quarterly spend of $20k. The Amex Personal Gold is another good choice, although even with the $50 OMA credit it is over $400 less in rewards.

Notable mentions were the Amex Business Aeroplan Reserve and the lower tier Aeroplan cards from TD and CIBC, but given that he already hold the TD AP VIP the benefit of these cards would be significantly reduced and the Amex MR is ultimately more flexible as it can be transfered to multiple programs (see my article on Why Amex is a good choice).

Hybrid Option

The next easiest the hybrid option where you combine a new card with a high earning card that you are already paying for the annual fee of. In this case, continuing with the Amex Business Gold, and only putting $20k on it to unlock the quarterly bonus before completing the spend on the already held Amex Business Platinum. This approach gives a very marginal benefit to the above one, with an unchanged cost, but about 4k more MR. With a value at $80 this may or may not be worth splitting the charge, and if you were going to split it, perhaps you'd want to consider a multi card approach.

Aggressive Treatment

Optimizing multi card approaches gets quite complex, particularly when you add in a spouse that can hold a duplicate card and SUBs that have multiple thresholds for returns. For example you could both open the Amex Business Gold, but should one of you target the 10k for $20k bonus, or should you just hit the first SUB and save the extra for more cards? A little trial and error is needed here, for this example we will assume that he has a spouse who can access any card (ie. good credit and no previous SUBs) except the OMA offers. I calculate the weighted value (ie. how much net benefit per dollar of spend) and then add them from highest to lowest weighted value to get the uber aggressive approach below:

Ten new credit cards and 11 transactions... this is more than a little crazy! For transaction costs of $700, annual fees of $1348 you'd get ~214k MR, ~129k Aeroplan, 106k bonvoy, and 52k scene points for a total net benefit pf pver $6k compared to the base case! Not to mention you'd get 2 free night credits with Bonvoy, a $50 OMA credit, 12-24 dragon passes (depending if you got free supplemental cards with the Scotia Passport VI) and your spouse would now have lounge access through their own CIBC VIP... as well as enough cards to fill a couple wallets.

I think this is a perfect example of why the "optimal" solution can't be a one size fits all. I think the one card approach is very reasonable in this case unless the patient was already considering getting some of these cards as keeper cards such as the Scotia Passport VI for no forex, or the Amex Bonvoy for free hotel stay credit. And if they're starting a clinic, surely there will be other opportunities for lump sum purchases, we don't need to engage in such a maximally complicated approach on this one.

See my note on how this changes as a business expense.

Case 2 - Cash Back on Forex

Presenting Complaint

Our patient has to pay a family member's tuition, this will be split naturally into three separate payments. The school interestingly does not charge a transaction fee for credit card payments, but we will have to consider currency exchange as it is charged in GBP. The purchase is for an intangible and as such credit card purchase protection is irrelevant. The estimated cost is 20k GBP split 10k, 5k, 5k.

Patient History

The currently have the Scotia Amex Gold, Scotia Passport Visa Infinite, Rogers Red World Elite MasterCard and HomeTrust Visa. They strongly prefer cash back, either directly or at least reliable point to cash conversion (ex. Scene+) and are not currently interested in accumulating points for the purpose of travel due to their current family situation precluding it.

Evaluating Treatment Options

Their preference for cashback over travel rewards guides us to assess Amex MR rewards at their statement credit value of 1cpp instead of their typical travel value of 2cpp, and to skip Avion and Aeroplan cards. Most Canadian credit cards charge a foreign exchange fee of 2.5% which creates a strong headwind for any cashback card to overcome, particularly since many offer only 1% back on uncategorized spend such as this and have lackluster sign up bonuses targeted at much lower spend amounts (ex. 10% back on first $2000 or $3000 with the Scotia Momentum and CIBC dividend cards). The Scotia cards which he already holds, and the hometrust card are both cards that do not charge foreign exchange fees. For the particularly motivated you could obtain US cards with no forex - the best of these are travel focused and as a result are not included. They also aren't a member of the OMA, so they don't have access to the unique Amex Personal Gold SUB structure.

Establishing the Baseline

Their base case was paying the full amount on their Scotia Passport Visa Infinite with no forex, a cost of $35,506 CAD and earning ~$355 worth of Scene points, an effective net cost of $35,151 CAD.

Single Card Option

Considering the above context we have the below comparison (non targeted rewards cards hidden), the Scotia Amex Gold and Hometrust are not shown as they have the same reward structure as the Passport VI and he has already received their SUB.

Even without a SUB available, the forex drag and cashback focus limit limit the performance of all but the Scotia Passport VI. If their spouse has not yet signed up for it, even better as you'd earn an additional $250 in Scene+ points SUB for a minimum spend of $1000.

A side note that the Rogers WE performance is dependent on being a Rogers customer (or related companies) and having their bills to redeem against. Seems like their base case was already a great choice, but was it the best one?

The base case was missing something key, it wasn't considering the possibility of involving the spouse. If the spouse hasn't yet opened any card, the best option is actually the Scotia Amex Gold with its more reasonable second tier SUB vs the Passport (Scotia Gold 25k at $1k and 20K at $7.5k, Passport 25k at $1k and 10k at $40k - ouch). Thanks to its first year free, even for non MDs, and no forex, this keeps our costs the same as our base case but gives us an extra $450 in SUB, even better if they sign up through GCR.

Hybrid Option

By reviewing the value of each card at their peak effective return, we find that the Amex Business Gold once again performs well, but not as well as the Spouse opening a Scotia gold (provided they haven't already)

If the spouse has already opened the gold, or if they want to try a two card approach, they would want to consider the business gold. But look closely, for some reason the $20k spend is not performing better despite its extra 10k points unlike the previous case- why? Lets think about what happens in the spend between the $5k minimum for the SUB and the $20k for that 10k bonus. You have to spend $15k more, earning 1x plus the extra 10k, thats 25k MR for $15k spend or 1.67x. At cashback value of 1cpp, this is 1.67% back - not enough to overcome the 2.5% forex. As a result the optimal target is at the $5k spend.

This gives us the ideal hybrid approach below if the spouse isn't getting the Scotia gold

Our costs have increased due to $121.95 in foreign exchange fees and $199 annual fee and we also earned about $50 less in Scene+. However, in exchange however we earned $750 in MR.

Or if the spouse can play too, we get the two card approach

We are now at approximately $800 better than the base case, not too shabby. But lets see how far we can take it, so that we can decide where in the range we want to end up.

Aggressive Treatment

The patient's preferences and previous card history doesn't lend itself well to aggressive treatment. Other than the Amex Business Gold the only other cards with net positive values are cash back cards with small SUBs for small minimum spends - hardly worth the effort. If however we can involve the spouse, I would put forward the below as the maximum.

If they did take part in this scheme though theyd end up almost $1500 better off than the base case. In terms of implementation I would split the first 10k GBP bill 2750 GBP on each of the business golds, and put the remaining 4500 GBP on the spouses scotia gold. The remaining bills I would pay with the Scotia Passport. In this way only the first transaction is "complicated" and the SUBs are all comfortably met.

Case 3 - Vacation Expenses

Presenting Complaint

Our patient is planning a series of expenses related to a trip to Spain. This will be split across numerous food, shopping and other purchases. Similar to case 2 this presents a forex but no transaction fee example. Notably different however is that numerous merchant interactions increase the probability of Amex acceptance issues which need to be considered in planning. Furthermore, any shopping that is for durable goods may benefit from credit card purchase protections. They anticipate a total cost in the neighbourhood of 20k Euro which represents a non-insignificant increase from their baseline spending.

Patient History

The currently have the Amex Cobalt, TD AP VIP, Rogers Red World Elite MasterCard and Costco CIBC Mastercard. They favour travel, and in particular would prefer Aeroplan points or MR points to convert to Aeroplan. Their spouse also has the TD AP VIP for the purpose of obtaining the SUB.

Evaluating Treatment Options

Based on this context we will use standard reward point values (ie. 2cpp for AP and MR) and favour them over unrelated travel points (eg. Bonvoy) and avoid Avion. Cashback cards are far weaker in this sort of a setup given their low earning rates.

The patient also expressed a strong preference for the simplest plan, so we definitely wont spend too much time considering aggressive options, however any Amex forward strategy should be backed up by a Visa or Mastercard as we don't have the same confidence that the whole spend will allow amex unlike a single vendor transaction.

Establishing the Baseline

Their base case was paying the full 20k Euro on their TD AP VIP, this would lead to $756 in exchange fees and produce 38.8k APP valued at around $776, a net positive of around $20.

Single Card Option

Considering the above context we have the below comparison (non targeted rewards cards hidden), the Scotia Amex Gold and Hometrust are not shown as they have the same reward structure as the Passport VI and he has already received their SUB.

Despite forex fees, the Amex Business Gold once again performs well for the single card approach at this spend level producing a sharp improvement over the base case with little effort.

The Amex Personal Gold OMA offer is also a strong candidate as it comes with an additional $50 OMA credit and 5x rewards on food up to $3000 which together add another ~$350 to the displayed value.

Honorable mentions to the Amex Business Platinum if lounge access beyond that provided by the AP VIP was attractive. If you were concerned about Amex acceptance and insisted on a single card approach, either opening a lower tier AP card, or the Scotia Passport VI could be considered (the free supplemental card and lounge passes would sway me to the Scotia).

Hybrid Option

The benefit of a hybrid option (ie. a single new card and another card or cards already held by the patient) in this case is that you can combine one of the Amex cards above with either the TD AP VIP or the Rogers WE to cover for amex refusals. Personally I would pick the AP card as I value AP higher than 2cpp, but if you have large Rogers bills I can see the appeal of the amplified cash back here. The difference in estimated outcome is small, but it is likely a better representation of the real work experience as it allows for over 1/3 of expenses to be paid for by the Visa during the trip.

Aggressive Treatment

For this patient, aggressive treatment has many options, but they expressly stated that they wanted to keep it simple. They might perhaps consider a 2 card approach, in which case I would swap the TDVIP in the hybrid with the Scotia Passport given its long term keeper status and easy to obtain SUB, plus you could get even more if you signed up through GCR.

For readers considering a more advanced plan, for this forex travel focused individual I would suggest they consider premium no forex US cards like the Bonvoy Brilliant. Also, there could be some optimization around including the already held Cobalt for food purchases up to its monthly cap given its incredibly high earning outpacing foreign exchange fees, provided they don't already max it out before or after their trip.

Case 4 - USD 47k lump

Presenting Complaint

Our patient has a large upcoming expense in USD. The vendor would prefer a wire and charges 3% fee for using credit cards. They may have the ability to apply for a US credit card via their spouse, but they don't have USD income so regardless would have to consider conversion of some form.

Patient History

Both they and their spouse hold the CIBC business AP Visa and personal AP Visa Infinite cards. They've recently lost their frequent flyer based lounge access, and have a family of 4.

Evaluating Treatment Options

In addition to the options used in case 3, we also could consider Marriott Bonvoy and US credit card products. Use of US cards eliminates the high credit card forex fee and instead allows us to use a low cost money changer, however the patient wasn't sure if this was something they wanted to pursue, and it is definitely is a more advanced approach so we will leave it to discuss another time.

Establishing the Baseline

They had initially thought they would use a no forex card for this purchase, but given the 3% transaction fee being greater than the return on the only canadian no forex cards, they would be better off using a low cost exchange like XE or Wise as their benchmark, with an implicit exchange fee of $792 or ~1.2% at time of writing.

Single Card Option

The combined headwind of 2.5% forex and 3% transaction fees is not surmountable with a single card at this spend range, and while the Scotia cards avoid forex fees, they only earn at 1%.

As a result almost all major Canadian cards perform worse than the base case when used as a single card. Notably the Rogers WE slightly outperformed with lower total costs of $672 vs the exchange rate implicit fee of $792. That said this is only for Rogers customers redeeming against a Rogers bill.

Even dual card approaches struggled to provide a meaningful positive return with the best case being the ever popular Amex Business Gold (net up $1300). I had hoped to identify an option involving platinum or VIP cards to give their lounge access back but it only turned notably positive when splitting the payment between two cards and a wire transfer (net up $1500 vs about $500 without the wire). Although ideally youd assign a value to the lounge access and other benefits to the platinum cards (eg. credits towards your cell bill).

Thankfully there is an ace up my sleeve - an additional layer I had hoped to not have to explore in this article due to length and complexity. We can modify the calculations to compensate for circumstances where the costs are business/pretax and the benefits are personal/post tax. This differential treatment of the cost vs the benefit gives a big advantage to strategies that are otherwise held back by their high costs, particularly the high annual fee cards. Ie. You could imagine that spending $800 of corporate money for $800 of personal benefit is preferrable to spending $100 of corporate money for $100 of personal benefit. In this example, if we apply a 50% relative discount to any fees paid by the corporation:

Fortunately this more than does the trick to dig some of the cards out of the hole even for a one card strategy. But since this patient was looking to split the cost evenly with their spouse, a dual card approach is logical.

Dual Amex business golds - spend $4k more corp spend for $4.5k personal worth of points

Dual Amex business platinums - spend $5.2k more corp spend for $4.9k personal worth of points and lounge access for 4 for a year.

Both of these offer a net benefit of about $3k vs the base case, and the platinums bring lounge access to the mix. Now thats more like it!

If this is not sufficient benefit, the return improves the more you're willing to split it up (eg. 2 cards and a wire, 4 cards etc).

Not explored here is the US issued credit cards for lumpy US expenses. If these are areas of interest to you we can discuss it more in your specific context.

Conclusion

I hope these four cases have given more colour to my approach for optimizing lump sums or temporary spend increases. The Amex Business Gold with the previously available sign up bonus was a strong performer in many of the permutations, as was the Scotia Passport Visa Infinite, unfortunately since writing this the spend requirement and bonus size of the business gold changed materially. However, the fact that they also could serve long term roles in your wallet make their case even stronger. Even without going to extreme measures one could unlock $1000-2000 in additional benefits by capitalizing on these lumpy spends.

That said, net value is only part of the picture, as case 4 showed us sometimes the benefits of lounge access prove a little too tempting!

If you need any help going through this exercise reach out for a free consult.

Referrals

To see the access the best offers for different Amex cards such as the Platinum click here. But if you're considering any business labeled Amex cards reach out!

The no forex of the Scotia Passport VI and Scotia Gold Amex make them both great choices for forex related lumpy spend. Other Scotia cards have this feature two and could be considered depending non scale of spend.

If you're on the fence, or wondering about other cards reach out to me for a free consult, and if you sign up for a card through my link, let me know and I will walk you through advanced tricks and personalized advice to help you get the maximum benefit both from earning and redeeming points - getting your travel journey going faster than you ever thought possible.

Check out my Keeper Cards series to see other cards worth exploring

Disclaimers

This should not be taken as financial advice and details are subject to change. I have made good intentioned efforts to be accurate but ultimately consult card terms and conditions and perform your own calculations.

Comments